Non-Profit

Maintaining Board Independence is Critical for Nonprofits

For nonprofit organizations, a board of directors is responsible for ensuring the organization upholds its mission, safeguards its assets, and operates in the public interest. While there are many legal, practical, and ethical reasons for a nonprofit to have a board of directors, the common theme is that it sets the foundation for good governance.

While many nonprofit board members are selected due to their ability to raise funds or strong ties to the organization’s mission, it’s also critical for nonprofits to maintain board independence.

What is board independence?

Independent directors are defined as those that are free from a conflict of interest. There are both state and federal laws that define when a conflict of interest arises.

Generally, it’s due to a director or family member having an interest that is different from that of the nonprofit organization. While usually the interest is financial, there are some states that have extended the definition to personal relationships.

In many circumstances, a lack of independence is limited to one specific transaction and doesn’t impact the director’s independence as it relates to the organization as a whole.

Ideally, directors are a source of wisdom, advice, and perspective for nonprofits. However, to effectively perform their role, board members must have relevant backgrounds, actively engage in governance of the organization, and be independent.

990 Reporting

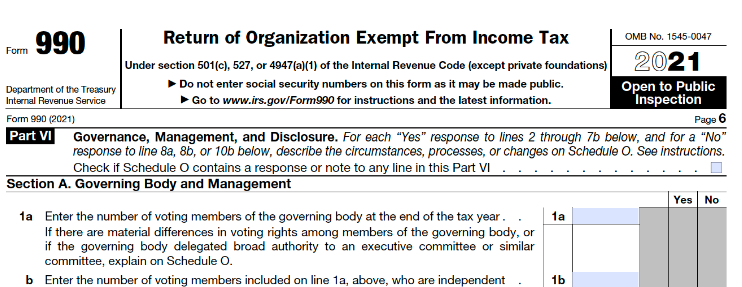

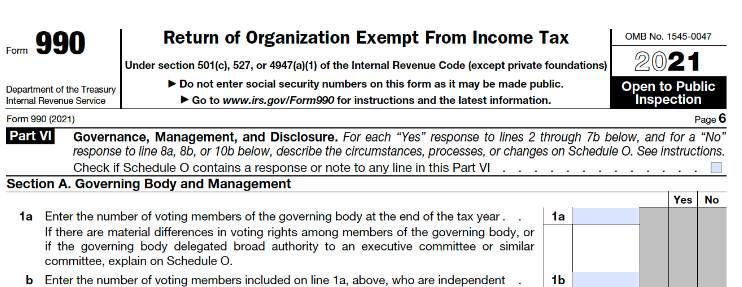

IRS Form 990, Part VI requires that nonprofit organizations report the number of (1) voting members and (2) independent voting members of a governing body.

Voting Members

The governing body is the group authorized under state law to make governance decisions for the organization and its shareholders or members, if applicable. Typically, the governing body is the board of directors or the board of trustees (or trustee).

In Form 990, Part VI, line 1a, the number of voting members of the governing body is reported. Only those members, as of the tax year end, of the organization’s governing body with power to vote on all matters (other than when disqualified by a conflict of interest) are included.

Additionally, if the governing body delegated authority to act on its behalf to another committee (e.g., executive committee, finance committee), the organization is required to describe the composition of the committee and the scope of its authority and indicate whether those committee members are also members of the governing body.

In Form 990, Schedule O, nonprofits can explain any material differences in members’ voting rights, the composition of delegated authority and its scope, and the number of committee members with delegated authority that are also members of the governing body.

Independent Voting Members

In Form 990, Part VI, line 1b, enter the number of independent voting members of the governing body as of the organization’s tax year end.

Members of the governing body are considered independent only if all of the following applied at all times during the tax year:

- They were not compensated as an officer or other employee of the organization (or a related organization). In addition, the member was not compensated by an unrelated organization or individual for services provided to the filing organization (or a related organization) if the compensation met the thresholds requiring reporting in Form 990, Part VII, Section A.

- They did not receive more than $10,000 of total compensation or other payments from the organization (or a related organization) as an independent contractor (other than expense reimbursements under an accountable plan or reasonable compensation for services performed in the capacity as a member of the governing body). The $10,000 threshold is based on the organization’s tax year (including a short year, regardless of whether the compensation is reported in Part VII of Form 990). Note: Reasonable compensation is determined using the Section 162 standards-for detailed coverage see Key Issue 34G in PPC’s 990 Deskbook.

- They (or a family member) were not involved in a transaction with the organization (whether directly or indirectly through an affiliated organization) that is required to be reported in the organization’s current tax year Form 990, Schedule L.

- They (or a family member) were not involved in a transaction with a taxable or tax-exempt related organization (whether directly or indirectly, through affiliation with another organization) of a type and amount that would be reported in Form 990, Schedule L, if required to be filed by the related organization.

Directors do not lack independence due to receiving reasonable (not excessive) compensation, being a donor to the organization, or receiving financial benefits from the organization solely in the capacity of being a member of the class served by the organization in the exercise of its exempt function [i.e., being a member of a Section 501(c)(6) organization], so long as the financial benefits comply with the organization’s terms of membership.

Practical Consideration: Lack of an independent governing body is often cited as one of the reasons the IRS may deny tax-exempt status to an organization.

Since 1974, our trusted advisors have partnered with nonprofit organizations to navigate every step of the financial journey. At Dugan & Lopatka, our CPAs and consultants are always on the cutting edge of changes in the nonprofit sector. We understand the challenges you face—the special accounting, auditing and reporting requirements of your organization—and we use our deep expertise to deliver exceptional service tailored to your needs.