Understand the changes you need to know, in minutes.

A new administration almost always means changes to the tax code, and Biden is no exception.

To view the report, scroll down.

(Note: Previously, we released a version of this report based on Biden’s campaign proposals. This new, updated edition is based on Biden’s more recent budget proposal, which gave us a clearer picture of the administration’s plans.)

The biggest changes:

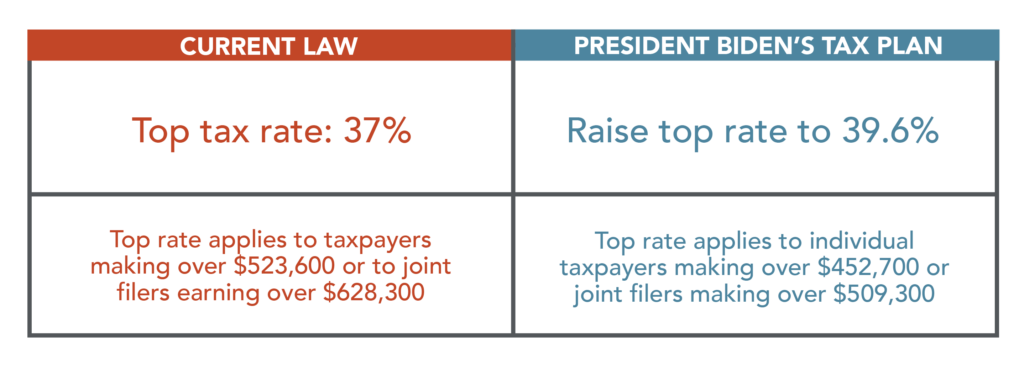

- Higher taxes for high earners, bigger breaks for lower incomes. The top bracket of the individual federal income tax rate is rising from 37% to 39.6% and expanding to include individuals making more than $452,700 and joint filers making more than $509,300. Meanwhile, taxes aren’t changing for individuals making less, while new credits and deductions are being added for lower- and middle-income individuals and families.

- Corporate tax hike. President Biden plans to raise the corporate tax rate from 21% to 28% and institute policies that prevent corporations from paying zero taxes.

- Made in America. The plan includes a number of provisions that reward businesses that bring jobs back to the U.S. and/or create new American jobs—and punish those that move overseas.

- Benefits for families. The maximum child/dependent tax credit will be raised from $3,000 to $8,000, and informal caregivers (including family members) will receive a $5,000 tax credit for medical care.

- Going all-in on green energy. The Biden Administration plans to end all tax benefits for the fossil fuel industry, while expanding incentives for renewable energy.

U.S. Individual Taxes

-

Individual Rates

Repealing the major tax reductions passed in 2017, President Biden plans to increase the top individual tax rate from 37% to 39.6%. He will also expand the bounds of the top bracket to include any individual taxpayers earning more than $452,700 or joint filers making over $509,300.

Based on a taxpayer’s income, the graduated tax rate is currently divided into seven brackets: 10%, 12%, 22%, 24%, 32%, 35% and 37%. Biden’s plan would apply to the top bracket (37%)—the taxpayers with the highest earnings.

However, the second-highest bracket (35%) currently applies to incomes over $400,000, and Biden has promised not to raise the income of people earning $400,000 or less. Therefore, his administration will have to adjust the income boundaries of the lower brackets.

Tax brackets are shifting. You may find yourself in a higher bracket for the first time, which may lead to changes in your financial strategy. -

Capital Gain Rates and Investments

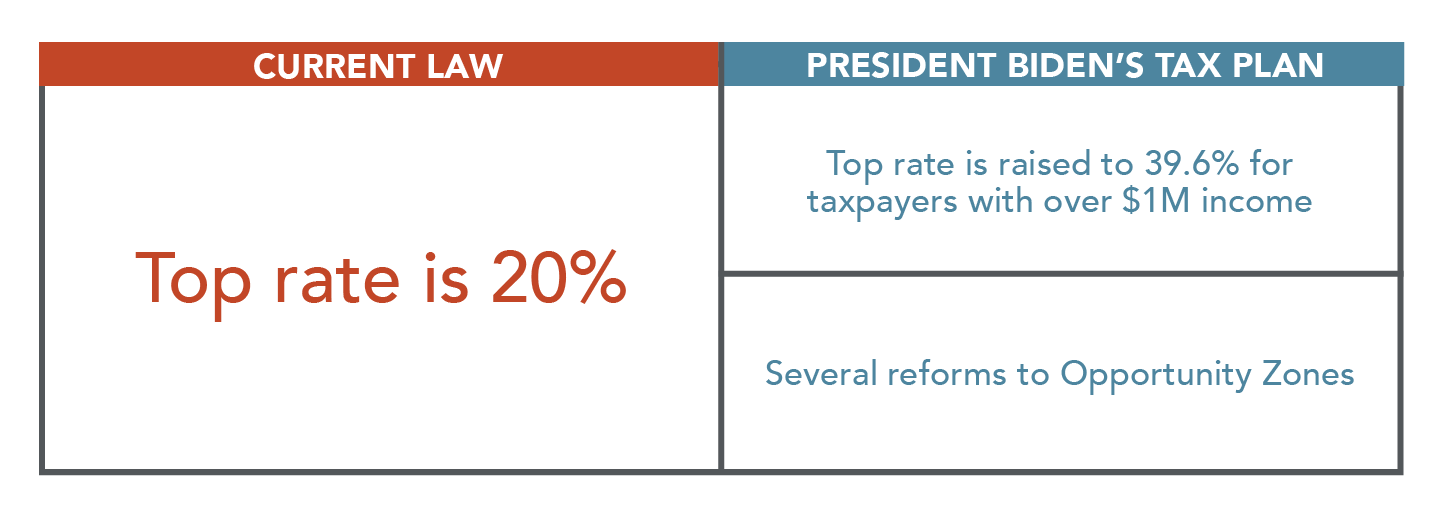

President Biden plans to raise taxes for top earners and introduce new incentives and oversight for investments in Opportunity Zones (economically distressed communities that qualify for tax deferment).

Currently, the top tax rate for capital gains is 20%. Net Investment Income Tax adds a 3.8% rate to joint filers earning over $250,000 and individuals earning $200,000. If you’re in the 10% or 12% tax brackets, you pay 0% for Net Investment. If you’re anywhere above the 12% bracket, you pay 15% for Net Investment.

Now, Biden plans to apply the top ordinary income rate of 39.6% for those earning more than $1 million. However, he clarifies that taxpayers can use the preferential 15% and 20% rates for capital gains until their total income reaches $1 million.

In addition, the administration is planning to incentivize taxpayers to partner with nonprofit or community-oriented organizations to jointly produce a community-benefit plan for investments. Plans should focus on making a direct financial impact on households within Opportunity Zones.

The Department of Treasury will review Opportunity Zone investments to ensure that tax benefits are only being allowed where there are clear economic, social and environmental benefits to the community. Also, recipients of these benefits will be required to provide detailed reporting and public disclosure on their investments.

If you could be impacted by the higher capital gains tax rate, monitor the legislation closely and consider recognizing some of your long-term gains before the new rates are enacted. -

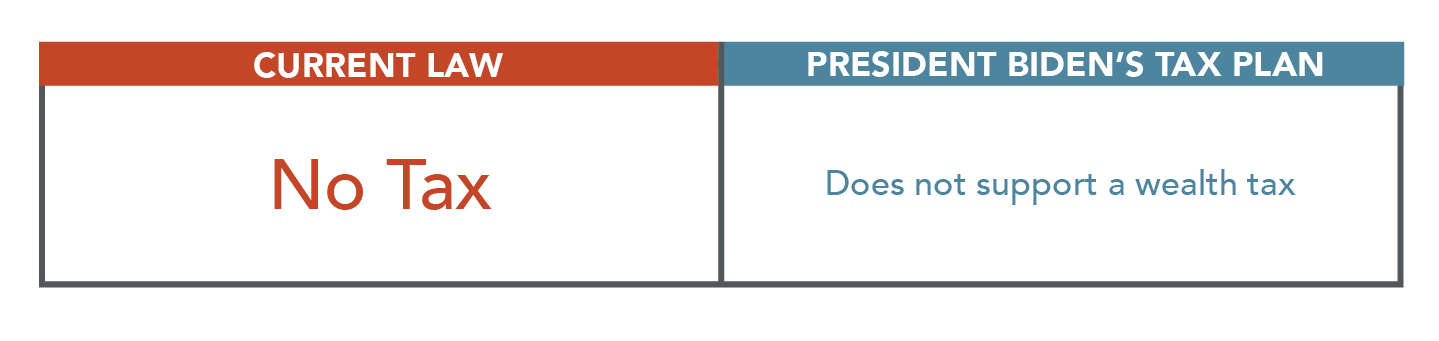

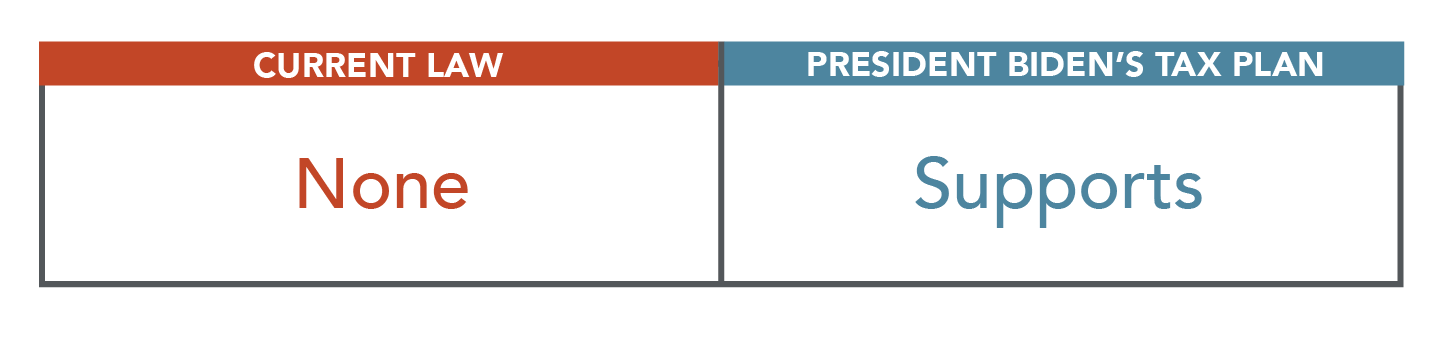

Wealth Tax

There isn’t currently a wealth tax, and there probably won’t be one in the near future. The Biden Administration has generally expressed that they do not support a wealth tax.

This is good news for the wealthy. However, high earners should expect to pay more taxes in general for capital gains and other income.

-

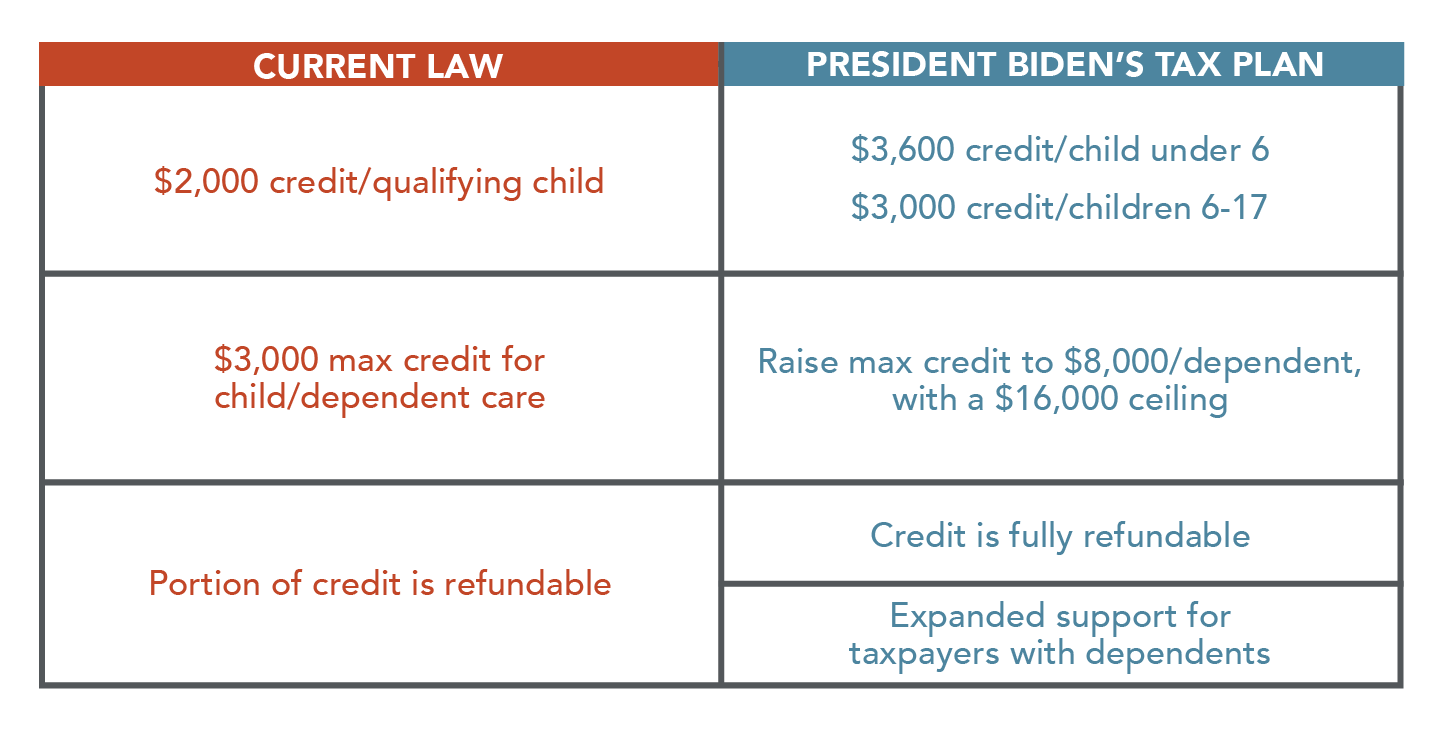

Child Incentives

President Biden plans to significantly expand tax credits for those with children or other dependents.

Currently, you can claim a $2,000 credit for each qualifying child and $500 for nonqualifying children or other dependents. A portion of the credit is refundable.

Under Biden’s plan, families will receive a tax credit equivalent to up to half of their spending on childcare for children under 13 (up to $8,000 for one child or $16,000 for two or more). The full 50% credit will be available to families making less than $125,000 a year, while families making between $125,000 and $438,000 will receive partial credit. This ensures that no families will receive less support than what they currently do.

The administration also plans to raise the child tax credit to $3,600 per child under 6 and $3,000 for children ages 6 to 17.

In March 2021, Congress passed the American Rescue Plan Act. The act increases the amount of the child tax credit to $3,000 per child ($3,600 for children under 6). The increased credit amount phases out for taxpayers with incomes over $150,000 for married taxpayers filing jointly, $112,500 for heads of household, and $75,000 for others, reducing the expanded portion of the credit by $50 for each $1,000 of income over those limits. The expanded child tax credit currently only applies to calendar year 2021.

Parents and caretakers in low- to middle-income households stand to receive dramatically higher tax credits.

-

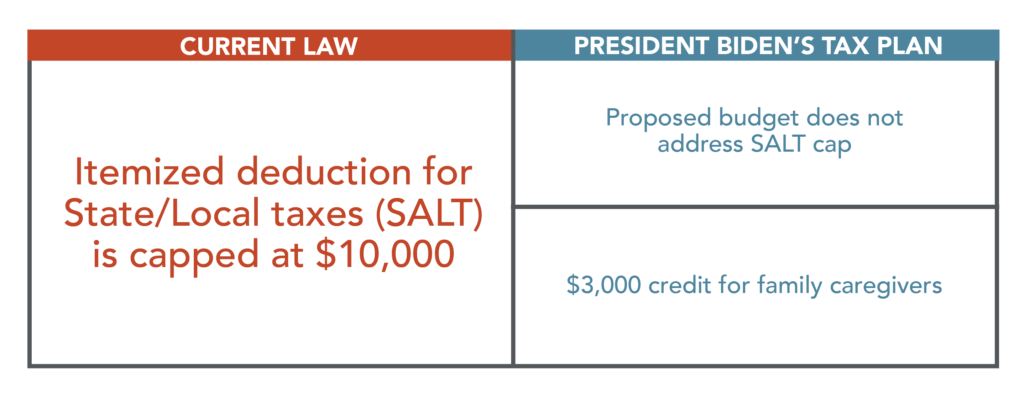

Credits and Deductions

The Biden Administration does not address the current $10,000 SALT cap on itemized deductions.

Biden proposed a $3,000 tax credit for family caregivers, to defray the cost of assisting a dependent.

Increased support for caregivers is a top policy priority of the Biden Administration and a recurring theme throughout the Biden Tax Plan.

-

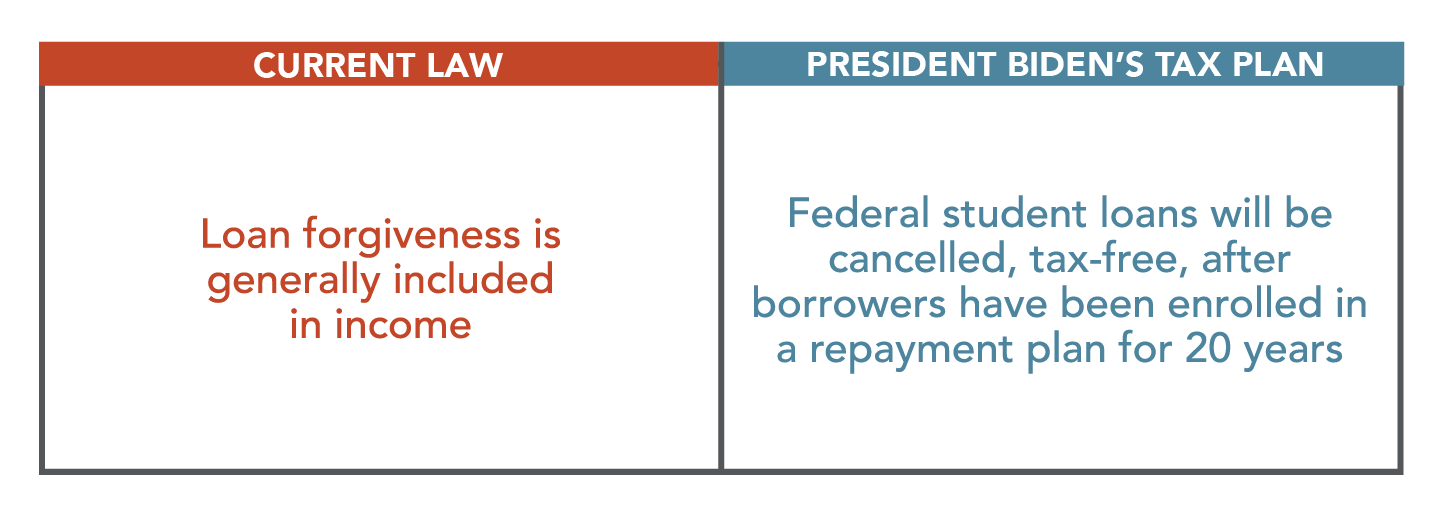

Student Loans/Education

The Biden Administration is taking steps toward forgiving (eliminating) some student loans. Under the Biden plan, federal loans will be cancelled, tax-free, after borrowers have been enrolled in an income-based repayment plan for 20 years.

But they may go further. Today, the administration is eliminating up to $50,000 of each taxpayer’s federal student loans.

So far, it’s unclear what form Biden’s loan forgiveness will take. It seems likely that it will happen, but those with loans should, for now, continue saving for repayment.

U.S. Business Taxes

-

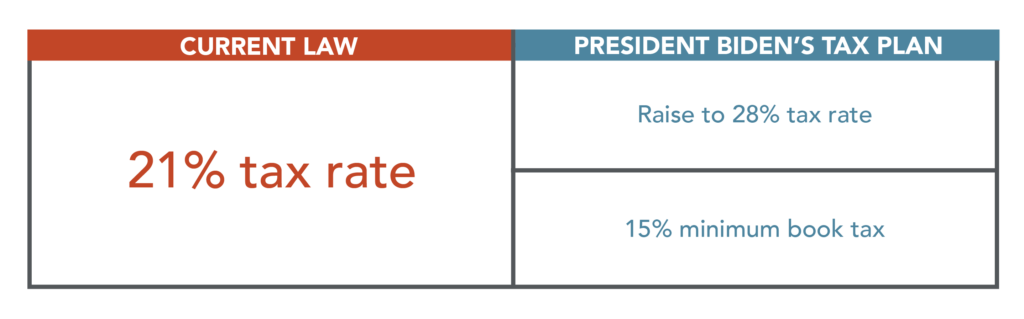

Corporate Tax Rates

President Biden has proposed increasing the corporate tax rate from 21% to 28%.

To prevent profitable companies from paying no taxes, corporations with profits over $2 billion that paid zero or negative federal income tax would be subject to a 15% alternative minimum tax (AMT) and liable for the greater of the regular tax or AMT. Credit for foreign taxes paid and carryovers are allowed.

Now is the time to evaluate how these proposed changes could affect your business or organization. For example, significant fixed asset purchases planned for Q3 and Q4 could be delayed until 2022 to receive a larger tax benefit.

-

Carbon Tax

While the Biden Administration’s current climate-change plan does not include a carbon tax, President Biden has previously expressed support for the policy. It’s likely a carbon tax will be instituted at some point in the Biden presidency, possibly within the first two years, with a Democrat-controlled house and senate.

Assume it’s going to happen. We know that Biden’s looking toward a carbon tax, so factor it into your planning if the carbon tax would impact your business.

-

Community Development

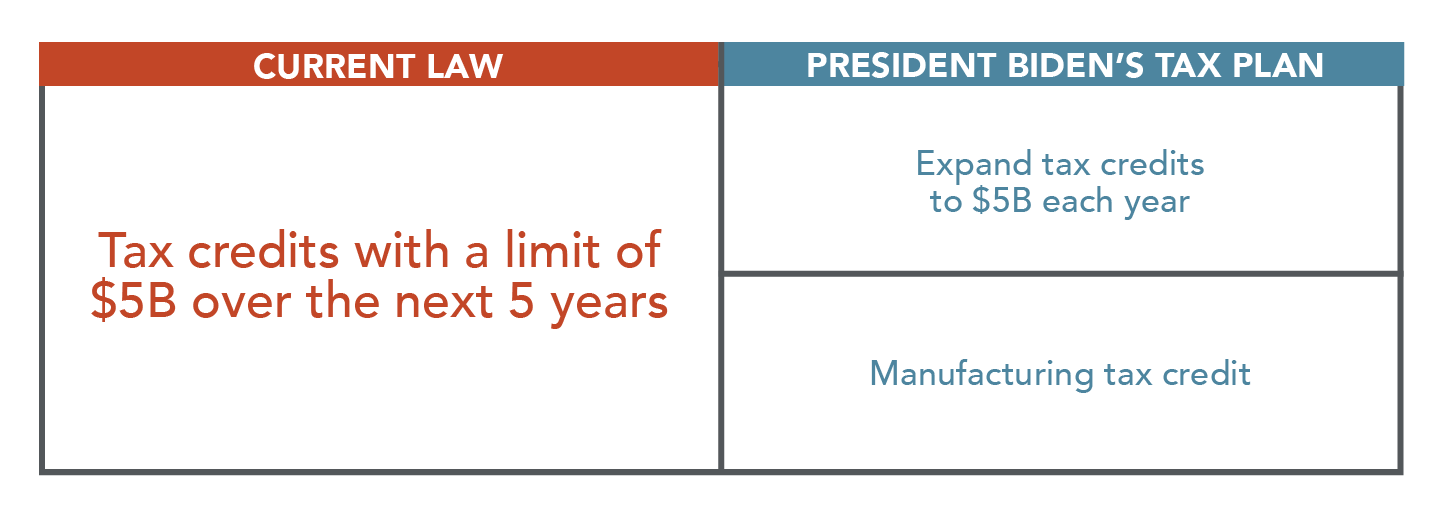

President Biden plans to drastically expand New Markets Tax Credits to spur development in economically distressed communities.

Today, if you make a qualified equity investment within the tax year, you can claim a New Markets Tax Credit. The current limit is $5 billion total for 2021-2025, and no amount can be carried past 2030.

Biden proposes expanding the current plan so that New Markets Tax Credits would provide up to $5 billion every year—and the program would be permanent. He also plans to enact a tax credit specific to manufacturers.

This is an aggressive move to attract private capital into low-income communities. If your business is considering an expansion/relocation, take a closer look at these incentives.

-

Credits & Incentives

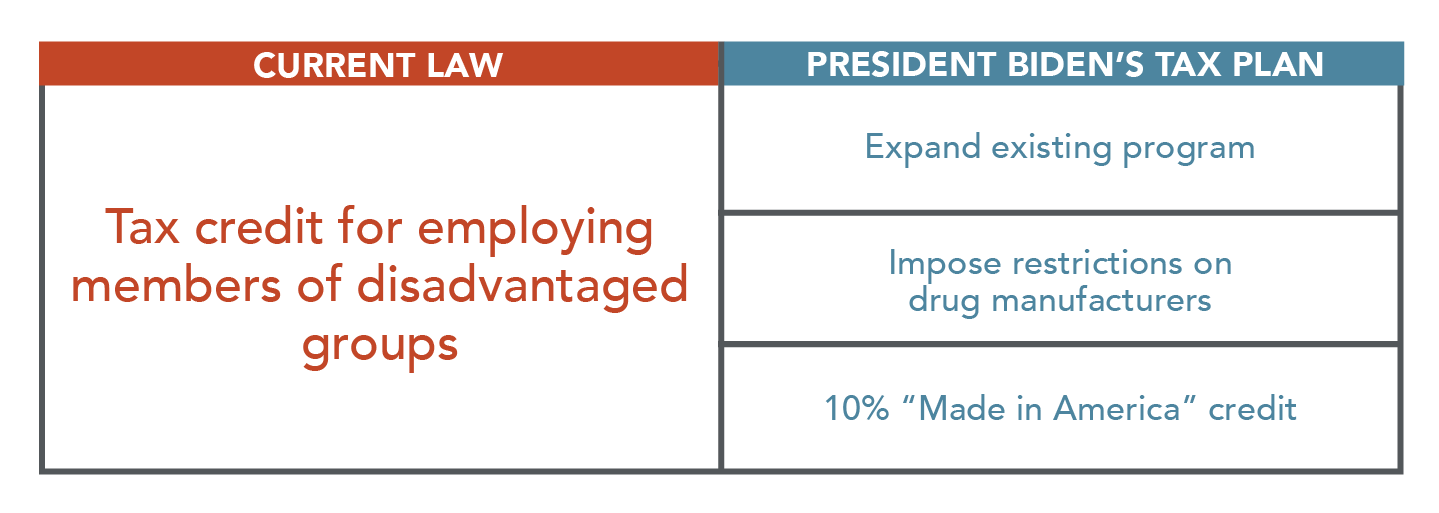

Currently, businesses enjoy a nonrefundable tax credit for a portion of wages paid to new employees who qualify as members of disadvantaged groups. The Biden administration plans to greatly expand incentive programs, with some restrictions for certain industries.

Under Biden’s plan, the Work Opportunity Tax Credit mentioned above will expand to include military spouses. A new childcare construction tax credit will encourage workplaces to build childcare facilities; employers will receive 50% of the first $1 million of construction costs per new facility.

Biden’s 10% “Made in America” tax credit will reward businesses that help create American jobs. This includes businesses that revitalize closed or nearly closed facilities, retool or expand American operations, and bring back production or service jobs to the U.S. This credit will also apply when a company increases manufacturing wages above pre-COVID levels (for jobs paying up to $100,000).

The Biden plan penalizes drug manufacturers that abusively raise prices over the generic inflation rate. Also, Biden plans to end the current tax deduction some pharmaceutical corporations receive for advertisement spending.

The “Made in America” tax credit is part of an overarching strategy by the administration to keep American businesses in the U.S. and encourage those that have left to return.

-

Fossil Fuels

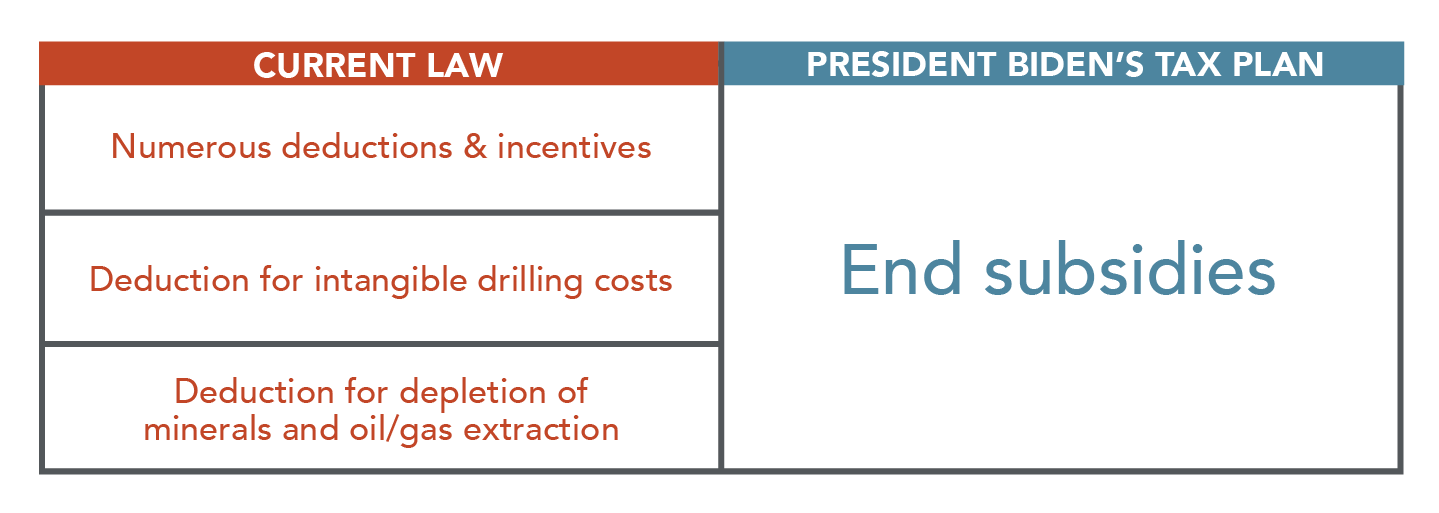

Biden proposes to end all subsidies for fossil fuel businesses, including deductions/incentives for drilling wells, depletion of oil and gas deposits and domestic manufacturing.

The Biden Administration is taking an aggressive stance against the fossil fuel industry. Businesses in this industry shouldn’t count on the incentives they usually receive. However, other incentives may push certain companies to invest in renewable energy.

-

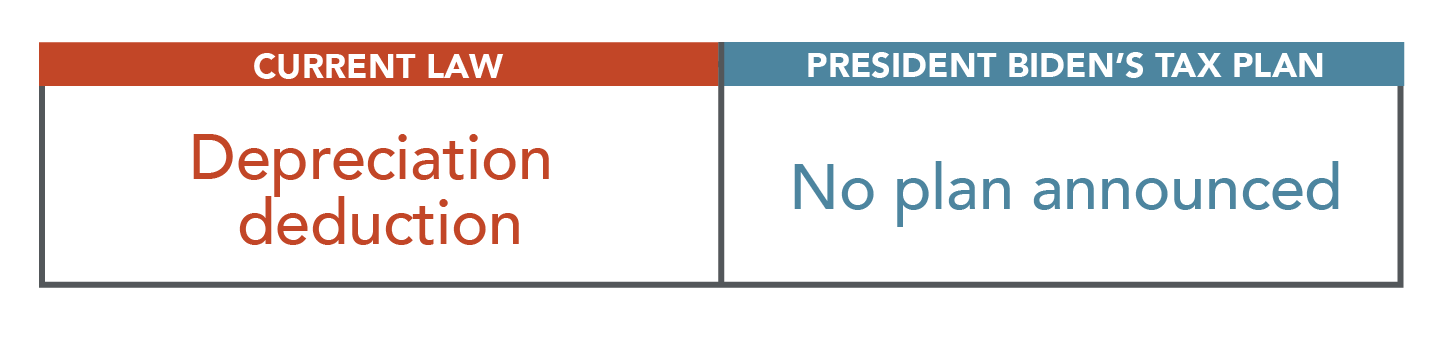

Depreciation

Currently, in order to recover the capital invested in an asset, you can deduct depreciation. During the first year of use, eligible property can be expensed entirely.

The Biden administration has not yet announced a plan related to depreciation.

This is a policy designed to encourage investment. It seems unlikely the Biden Administration will change it while trying to revive a post-pandemic economy. However, the area most likely to be addressed would be how long 100% bonus depreciation remains available.

-

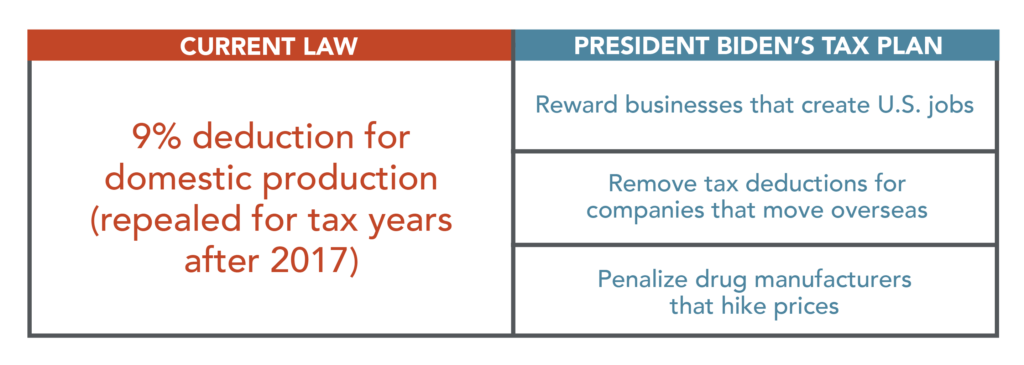

Manufacturing

Previously, businesses received a 9% deduction for domestic production activities. This was repealed by the Trump Administration for tax years beginning after December 31st, 2017.

The Biden Administration plans to reward businesses that bring manufacturing jobs back to the U.S. and/or create new jobs in the States with a 10% tax credit. Meanwhile, Biden will remove tax deductions for expenses incurred in connection with moving jobs overseas.

The plan includes a provision to penalize drug manufacturers that abusively raise prices over the general inflation rate.

This is part of Biden’s strategy to keep American companies in the U.S. and bring jobs back to the manufacturing sector. Here and elsewhere, there are policies that punish drug manufacturers that practice what this administration considers unfair practices.

-

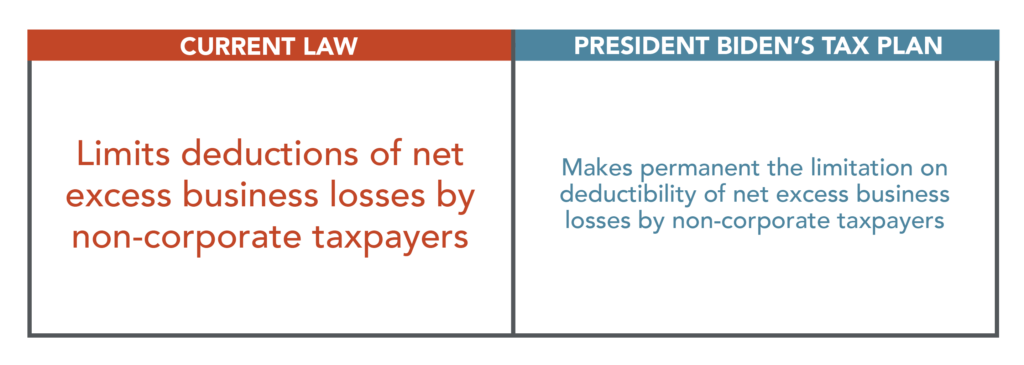

Excess Business Losses for Non-Corporate Taxpayers

Currently, there are laws that limit the amount of money you (a non-corporate taxpayer) can deduct based on net excess (or ‘non-passive’) business losses. These laws limit married individuals who are filing jointly from deducting more than $524,000, while individuals can’t deduct more than $262,000 based on business losses.

These limitations were set to expire in 2027, but Biden plans on making them permanent.

The bottom line of Biden’s plan, here and elsewhere, is that higher-income individuals and corporations will pay higher taxes. This provision goes hand in hand with increasing the corporate tax rate to effectively level the playing field between entities.

-

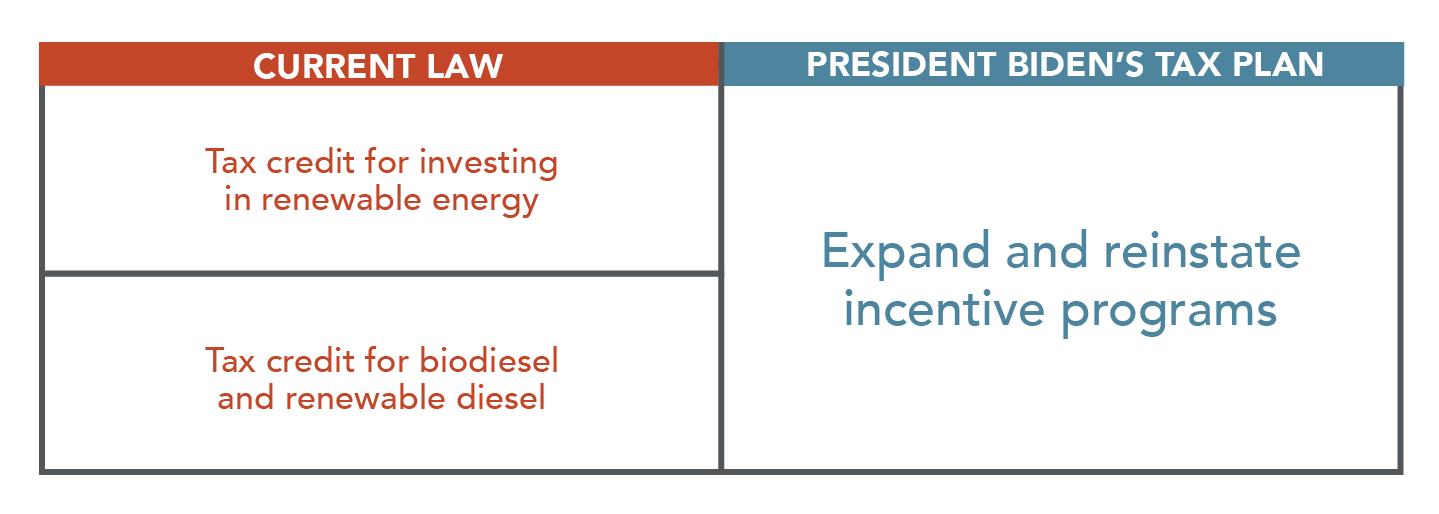

Renewable Energy

President Biden plans to significantly expand renewable energy incentives and reinstate certain programs.

This includes:

- Restoring the full electric-vehicle tax credit.

- Expanding deductions for investments that reduce emissions in commercial buildings.

- Reinstating tax credits for residential energy efficiency.

- Reinstating the Solar Investment Tax Credit (ITC).

- Creating tax benefits for carbon capture, use and storage.

While Trump rolled back numerous programs aimed at encouraging sustainability, the Biden Administration is making green energy its top priority. You can already see the impact of this with GM’s investment in electric vehicles.

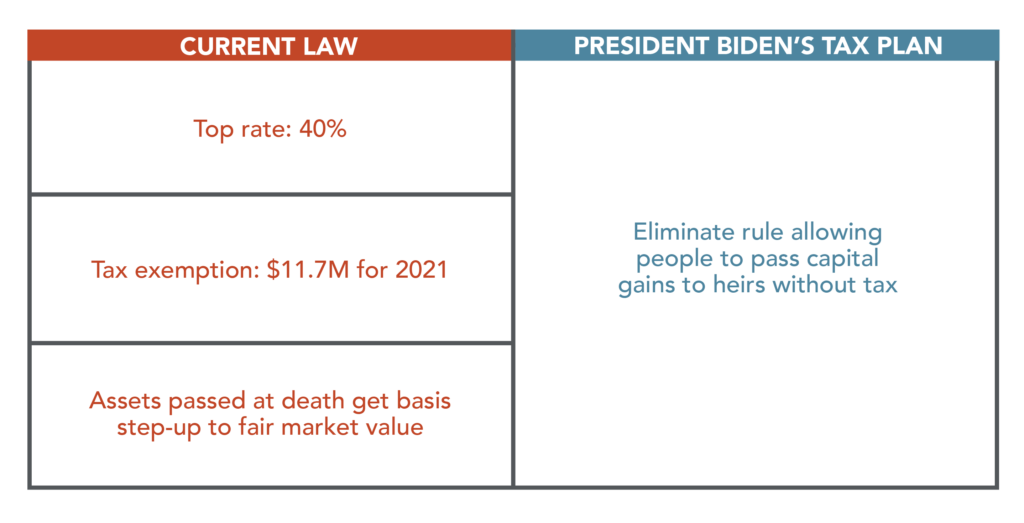

Estate Taxes

-

Estate Taxes

Currently, following an individual’s death, heirs receive a step-up in the tax basis of the assets they inherent equal to the fair market value of the asset at the time of the decedent’s death. This effectively allows the heirs to inherit assets without paying income tax on the appreciation. That’s likely to change.

Under Biden’s proposed budget, the donor (or deceased owner) would realize capital gain at the time of the transfer to beneficiaries. In other words, the tax would now apply to gifts and assets transferred to heirs following an individual’s death. This comes with a proposed $1 million exemption.

Additional exclusions include:

- Transfers to a U.S. spouse or charity

- Exclusion for up to $500,000 per couple for any capital gain on a principal residence

- Certain family-owned businesses

Currently, there are no plans to directly increase the estate tax.

It’s still unknown whether or not Biden will revive the Obama-era plan to eliminate the discounts on transfers of family-owned businesses. These court approved valuation discounts can significantly reduce the estate tax liability.

Financial Instruments and Transactions

-

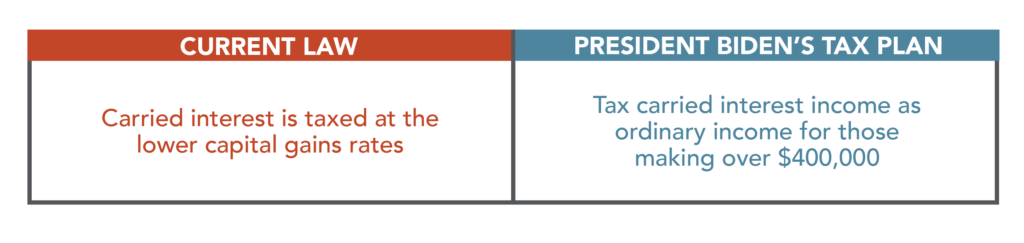

Carried Interest

Currently, the income received by the general partner of a private investment fund (“carried interest”) is taxed at the lower capital gains rates. President Biden plans to tax carried interest income as ordinary income for partners with taxable income over $400,000.

Carried interest has long been a loophole for investors, particularly private-equity and hedge-fund managers. If you’re in this group, you will now have to pay ordinary income tax on your investment income (which translates to significantly higher rates).

-

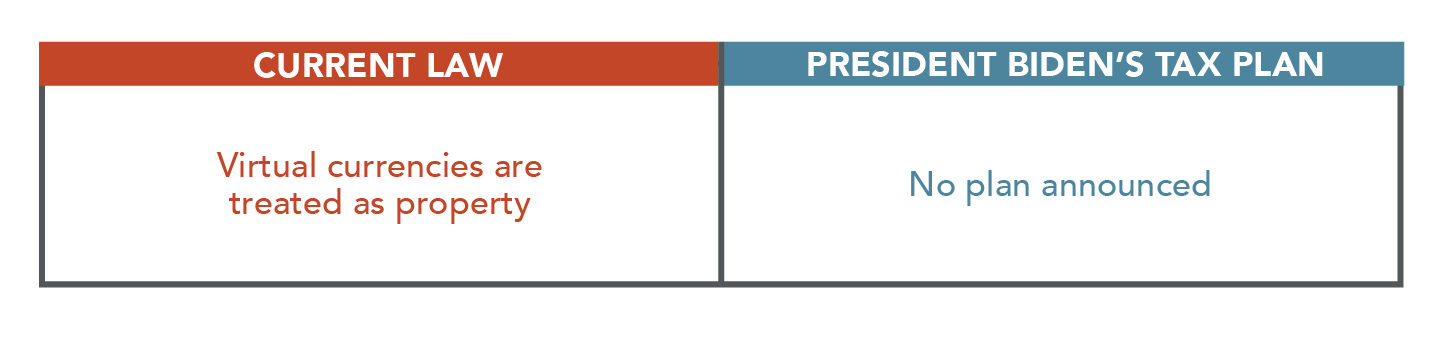

Cryptocurrency

While cryptocurrency is becoming increasingly popular, the Biden Administration has not yet announced related tax reforms. Today, the IRS requires taxpayers to report ownership of virtual currencies on their Form 1040. This currency is treated as property, for tax purposes.

However, Biden’s budget does expand the scope of information reporting by brokers who report on crypto assets.

President Biden has yet to directly address cryptocurrency. But, as currencies like Bitcoin become more popular, it seems only a matter of time before the federal government adjusts its policy.

-

Transaction Tax

President Biden has expressed support for the taxing of certain financial transactions, such as the buying or selling of stocks, bonds and/or derivatives. There is currently no such tax.

A transaction tax could have a major impact on the way people invest in the U.S. economy.

Real Estate

-

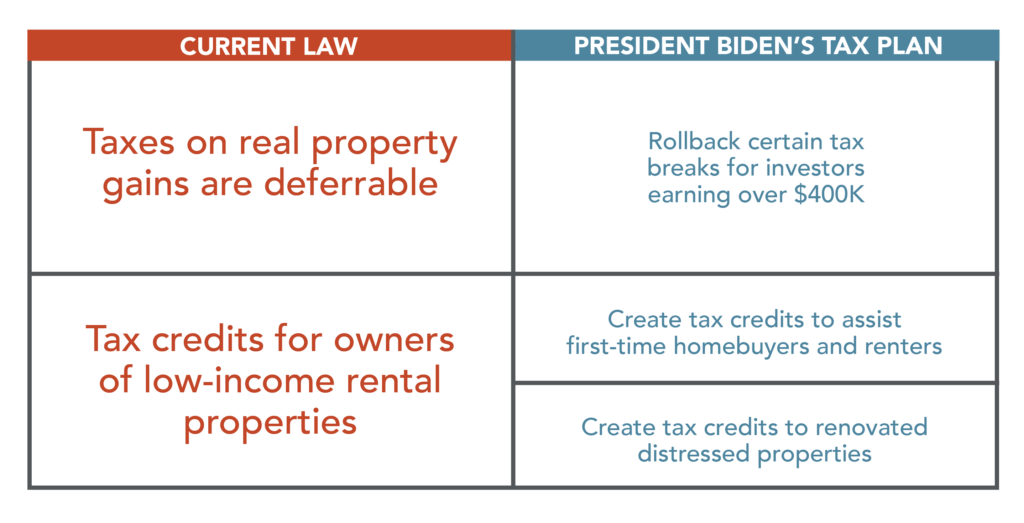

Real Estate

Today, you can defer taxes on gains of real property if you’ve exchanged the property for that of “like-kind” (a property considered equivalent). President Biden’s proposed budget would allow the deferral of gains up to $500,000 for each taxpayer ($1 million for married individuals filing jointly) each year for property exchanges that are like-kind. Any gains in excess of these amounts would be taxable in the year of the exchange.

President Biden plans to roll back certain tax breaks for real-estate investors making more than $400,000.

Biden plans to create a tax credit of up to $15,000 (refundable and advanceable) to assist first-time homebuyers, as well as a Neighborhood Home Credit program to encourage businesses to renovate properties in financially distressed communities.

While Biden’s proposed changes to tax deferment on real property will not affect the majority of Americans, wealthy individuals should consider potentially higher taxes when exchanging properties in the future.

Tax Enforcement

-

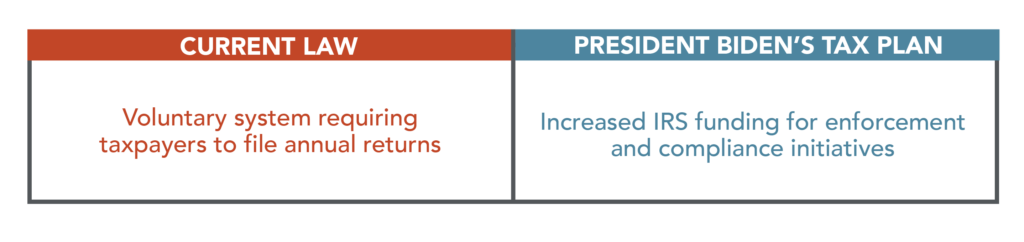

Tax Enforcement

The Biden Administration is proposing increased funding for the IRS for enforcement and compliance initiatives, as well as funding to enhance information technology capabilities.

Today, the IRS collects $440 billion LESS than it is owed. The additional funding will help reduce this ‘tax gap’.

Compensation and Benefits

-

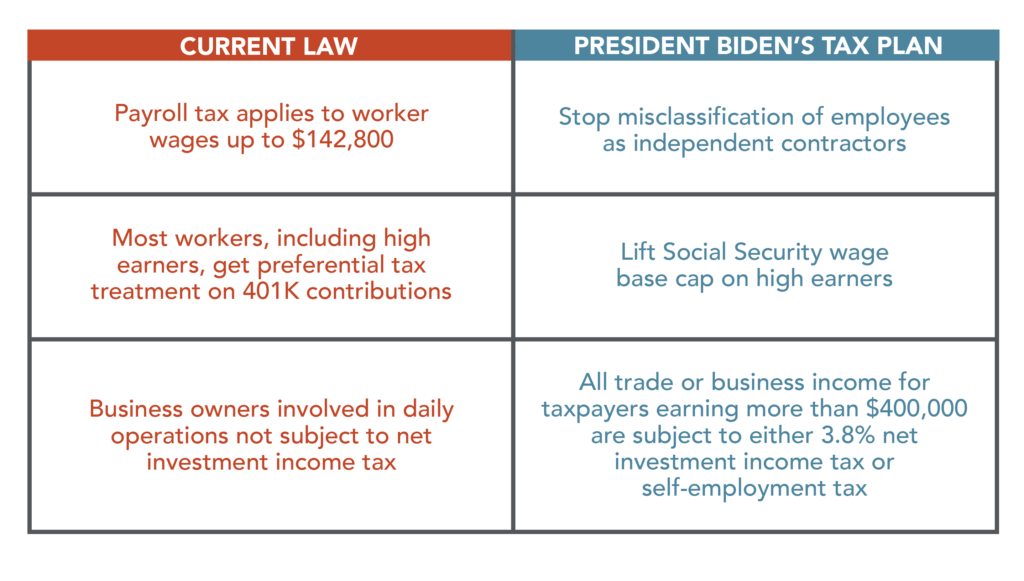

Employment/Social Security Taxes

Today, some employers deliberately misclassify their employees as independent contractors, allowing them to avoid paying employment taxes. The Biden Administration has vowed to stop this.

President Biden also plans to raise the Social Security taxable wage base cap on high earners—requiring individuals making over $400,000 to pay higher taxes for their contributions. Under the new plan, those earning $400,000 or less will not pay additional Social Security taxes.

Currently, business owners involved in daily operations are not subject to the net investment income tax on their share of the taxable income from the business. However, under the new Biden Tax Plan, all trade or business income for taxpayers earning in excess of $400,000 would be subject to either the 3.8% net investment income tax or self-employment taxes.

The Biden administration has drawn a line at $400,000: Those earning more will pay higher taxes, while those earning less will pay about the same taxes and find themselves eligible for more incentives. Individuals who are just over the $400K mark may find themselves in the highest tax bracket for the first time.

-

Health Care and Long-Term Care

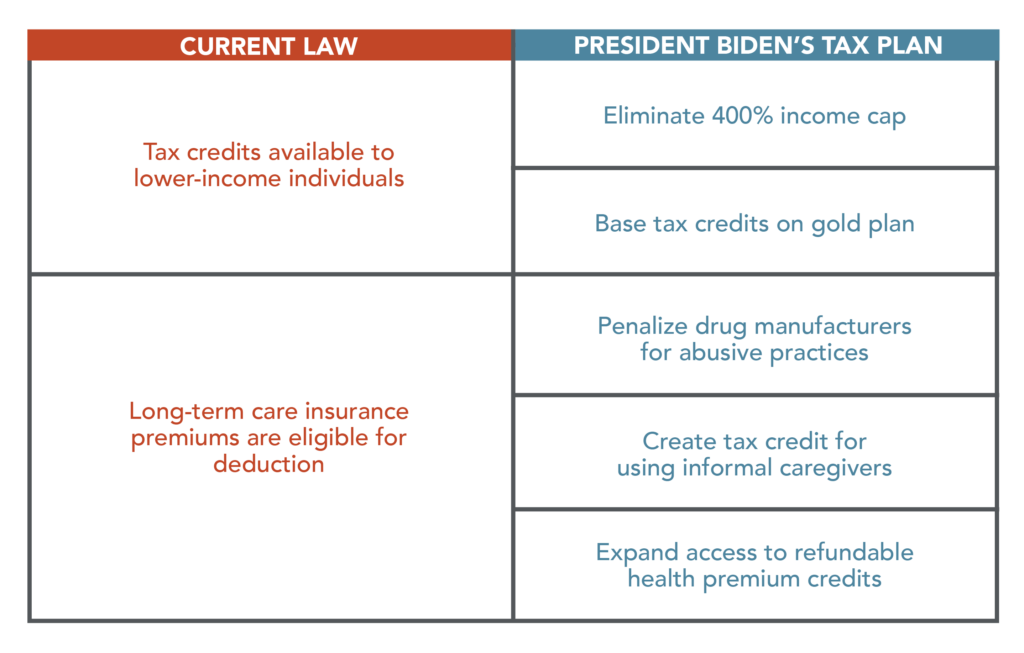

President Biden plans to eliminate the 400% income cap on tax credit eligibility for the premium tax credit. Credits will now be based on the gold plan (rather than silver).

The Biden plan also penalizes drug manufacturers that abusively raise prices over the generic inflation rate. Biden plans to end the current tax deduction some pharmaceutical corporations receive for advertisement spending.

Under the new plan, informal caregivers (including family members) can receive a $5,000 tax credit, and tax benefits will increase for older individuals who purchase long-term care insurance using retirement savings.

Biden plans to expand access to health premium tax credits (refundable), in order to ensure that families do not spend more than 8.5% of their income on health insurance.

Make sure you know the tax credits you should be receiving. Too often, people and businesses leave credits on the table.

International Business Taxes

-

BEAT/GILTI

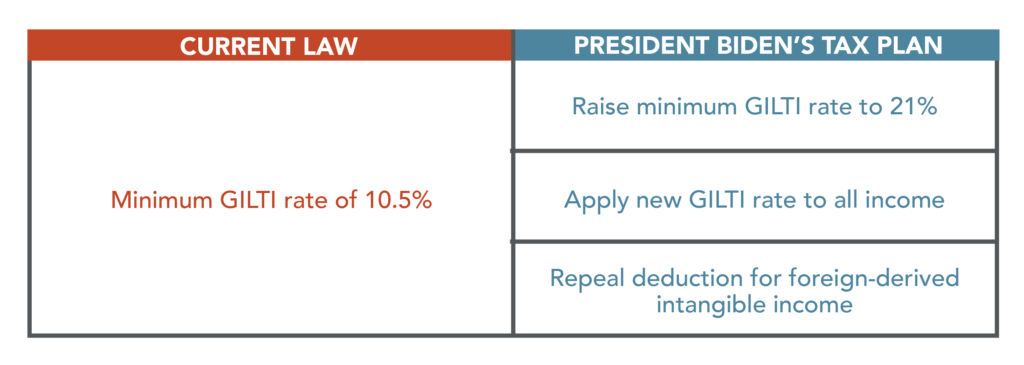

For U.S. shareholders of CFCs (controlled foreign corporations), there is currently a minimum tax rate of 10.5% on global intangible low-taxed income (GILTI). President Biden plans to double this rate to 21% and apply it to all business income brackets. Furthermore, Biden proposes repealing existing deductions for foreign-derived intangible income.

Currently, the minimum BEAT (base erosion anti-abuse tax) is set at 10% and 12.5% for tax years beginning after 2025. President Biden’s proposed budget would repeal BEAT with a new “stopping harmful inversions and ending low-tax developments” (SHIELD) rule.

Here, the Biden Administration is taking aim at shareholders who have managed to pay low U.S. taxes in the past.

-

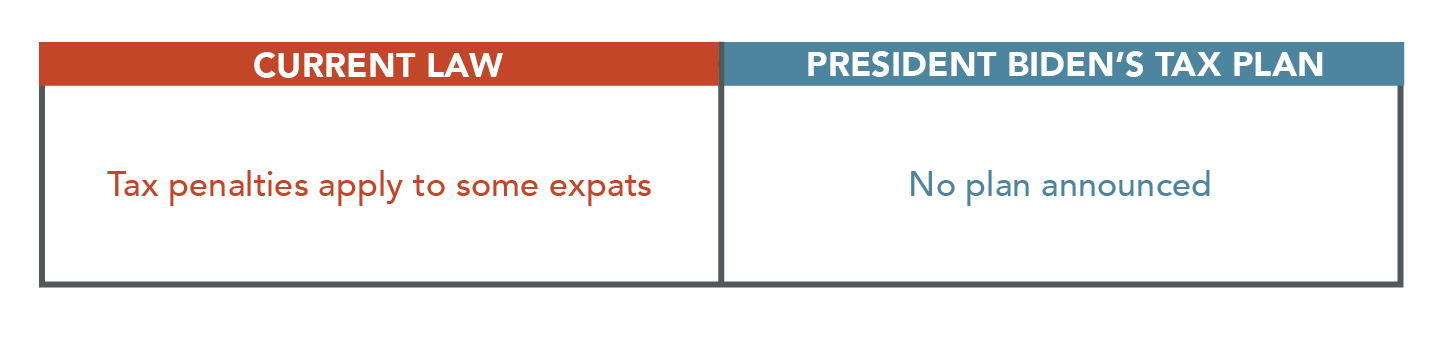

Expatriation

Today, Americans who renounce their citizenship—as well as certain long-term resident aliens who terminate their resident status—may face special “mark-to-market” taxes. The Biden Administration hasn’t announced any plans to change this.

-

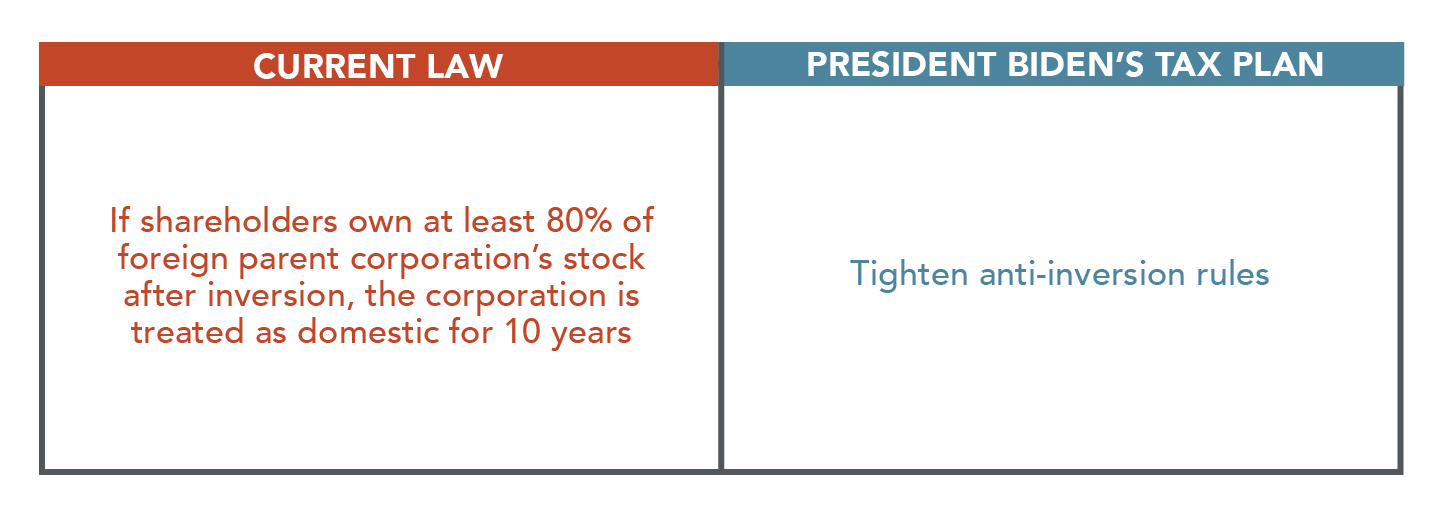

Inversions

The Biden Administration is cracking down on corporate inversions: a maneuver in which shareholders of a corporation transfer stock to a foreign-owned subsidiary in exchange for newly issued shares of the subsidiary’s stock.

Currently, if shareholders own 80% or more of the new foreign parent corporation’s stock after the inversion, the parent corporation is treated as a domestic corporation for all federal tax purposes for ten years. President Biden is expected to tighten these anti-inversion rules.

This is the administration closing another loophole that has allowed certain shareholders to avoid paying U.S. tax.

-

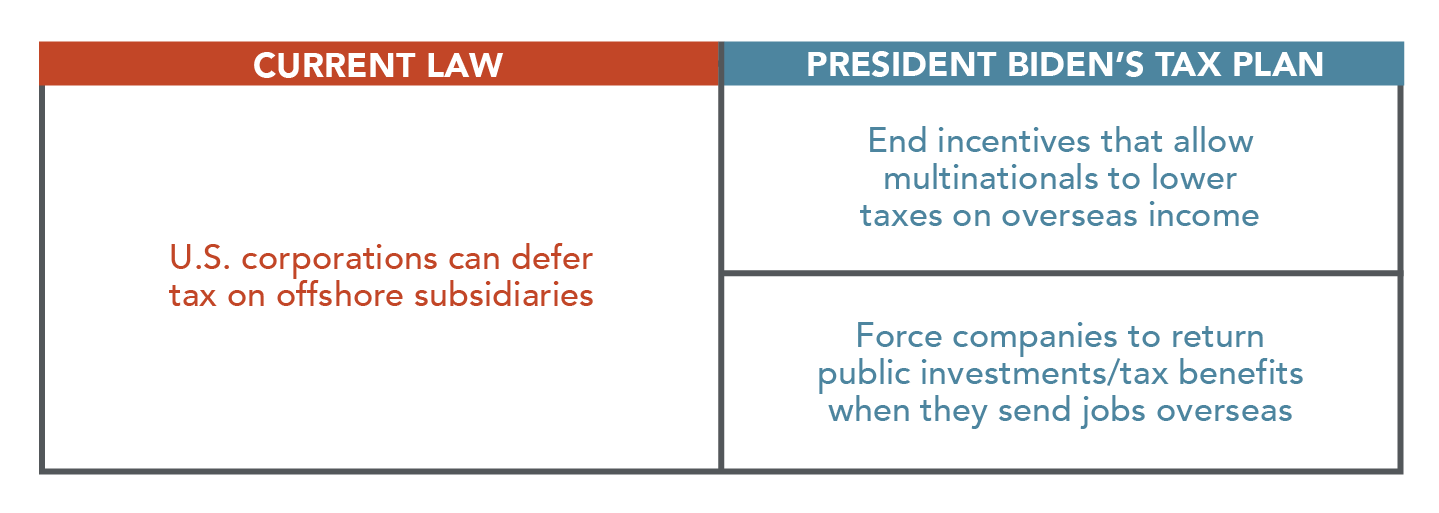

Repatriation

Many of Biden’s new policies aim at keeping businesses (and their money) in the U.S., and this is no exception.

President Biden plans to end incentives that allow multinational corporations to drastically lower their taxes on income earned overseas (in some cases, these incentives have allowed the most profitable companies to pay no tax at all).

He also plans to establish “claw-back” provisions. If a company sends American jobs overseas, these policies will force the business to return public investments and tax benefits.

The “claw-back” policies aim to penalize companies that move overseas, particularly those that have received significant benefits in the past.

-

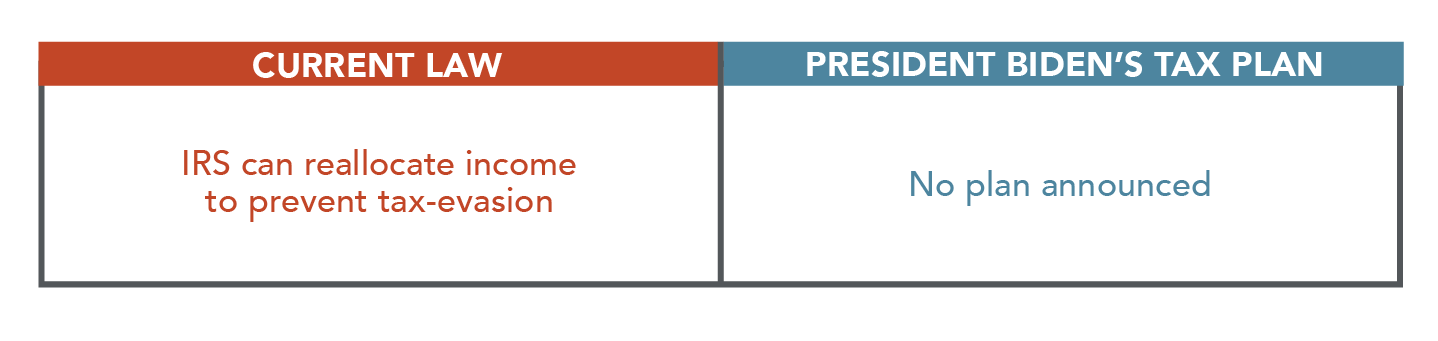

Transfer Pricing

Currently, the IRS can re-allocate income and other items among related policies to prevent tax-evasion or to clearly reflect income. President Biden has not announced any plans to change this.